Available in

Related countries

Introduction

Many African economies face important financing needs, making the development of vibrant and well-functioning domestic capital markets a priority across the region. Stronger market-based finance could help spur innovation and competitiveness, improve financial inclusion, and drive sustainable growth.

Several African countries have made strides in improving their capital market ecosystem but progress remains uneven. Many markets continue to face significant challenges, including limited market infrastructure and liquidity, shallow investor bases, and regulatory fragmentation. These constraints may also limit their ability to close climate transition investment gaps and fully support economic growth.

The Africa Capital Markets Report reviews the policy and regulatory environment for debt and equity markets in the region, and provides guidance to help authorities strengthen them.

Capital markets in Africa are generally less developed than in other regions

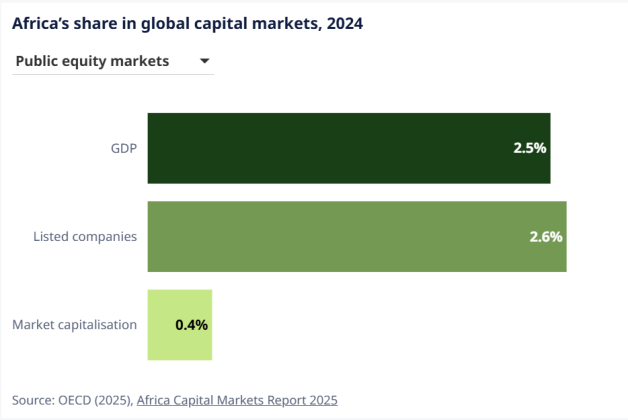

African companies account for only 1% of the total value of equity raised globally since 2000. Capital market activity is highly concentrated, with South Africa, Morocco and Egypt accounting for 80% of total market capitalisation, and trading activity is generally low. Weaknesses in the corporate governance of listed companies and of state-owned enterprises limit their contribution to capital markets. Digital financial services have expanded financial inclusion but more investment in digital technology would increase their impact on capital market activity.

Sovereign and corporate debt markets are underdeveloped

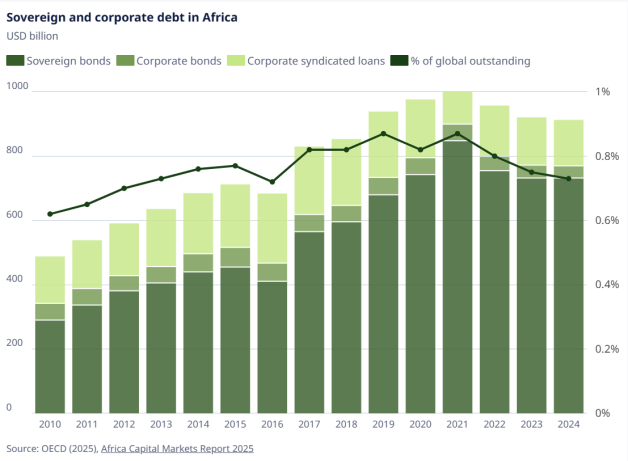

Africa accounts for only 1% of global sovereign bonds, lower than its 3% share of global GDP. Combined with large refinancing needs, this is straining the fiscal capacity of many countries. Corporate debt is also low and accounts for just 5% of total EM corporate debt, with activity highly concentrated in a few countries. Both sovereigns and corporates are exposed to significant foreign currency risk as a large part of their debt is denominated in foreign currencies. 80% of rated African countries are classified as high or very high risk.

The small size of institutional investors limits the investor base

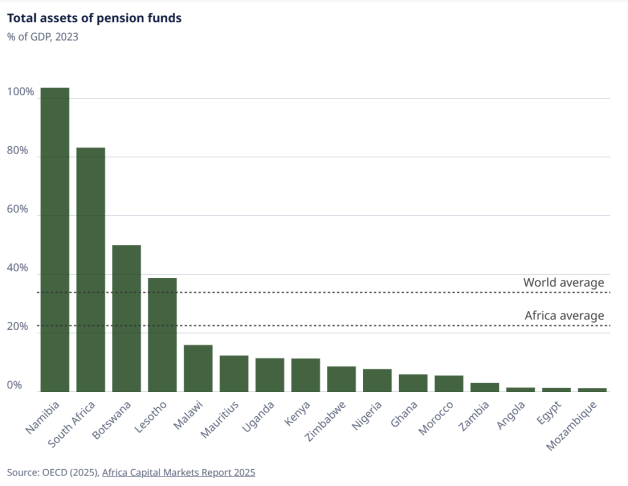

Insurance companies and pension funds play a limited role as institutional investors in most African countries. Insurance penetration, at 3.5% of GDP, is half the global average, and pension fund assets are also smaller, equivalent to 23% of GDP compared to 34%. The limited size of their assets and considerable allocation to government assets prevent them from contributing as stable providers of capital to the real economy. For pension funds, low incomes and high levels of informal employment present additional constraints.

The climate transition in Africa faces a major financing gap

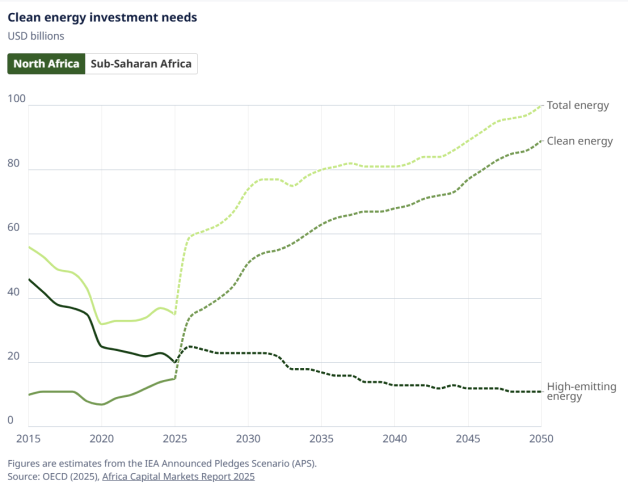

Assuming recent trends in public and private climate investment in Africa, shortfalls in climate investment are expected until 2040. While investments grew by 15% annually during the last 3 years, clean energy investment must rise to 2.4 times current levels in North Africa and 1.8 times in Sub-Saharan Africa to meet the required 2026 targets. This highlights the importance of the involvement of both public and private sectors to achieve climate goals.

What can governments do?

Strengthen capital market activity

Creating flexible listing frameworks and improving transparency could help attract more issuers. Digitalising trading infrastructure and supporting regional capital market integration could promote cross-border activity and lower operational costs. Stronger board independence, transparency and minority shareholder protection would help improve investor confidence. Integrating SOE governance reforms within broader market development could catalyse private sector growth.

Deepen local bond markets

Mitigating financial vulnerabilities, developing long-term borrowing strategies, and improving co-ordination across fiscal, monetary and regulatory policies are essential to develop local bond markets. Prudent debt management and a gradual shift toward greater reliance on local currency-denominated bonds are also critical. Measures to enhance liquidity, reduce costs, and diversify the investor base could be considered.

Develop the role of pension funds and insurance companies as institutional investors

Strong and transparent frameworks are needed to strengthen the role of institutional investors in capital markets. Measures could include enhancing the protection of insurance policyholders' interests, increasing pension participation through automatic enrolment, supporting portfolio diversification, and facilitating long-term investments. Deeper regional integration and better interoperability between market infrastructures would also help expand the pool of investors.

Leverage debt markets and private sector investment for the climate transition

Further integrating African capital markets would help mobilise funds for the climate transition by expanding investor bases, leveraging underutilised liquidity, and broadening investment options. Sustainable bonds, critical for financing this transition, could be a particularly useful instrument for energy companies.

Support responsible AI deployment

Further investment in AI-enabling infrastructure, research and development, and human capital, supported by robust regulation that balances innovation with consumer protection and market stability, is needed. At the same time, AI models must be trained on locally sourced, representative data to reflect the continent’s linguistic, cultural, and socio-economic diversity.